First in a series examining how the United States manages- and could better manage- its critical minerals strategy

The US sits at a strategic inflection point with critical materials. A subset of these critical materials are critical minerals, needed to make the likes of F-35 fighter jets, electric vehicle batteries, and smartphone displays, and they are increasingly concentrated in the hands of rivals, particularly China. Washington has responded with a patchwork of lists, policies, and programs, but the underlying frameworks for deciding which minerals matter, how much they matter, and what to do about it remain undercoordinated and insufficiently rigorous.

This is the first in a series examining the state of U.S. critical minerals policy. We’ll take a look at the current policy landscape and propose enhancements through a risk/opportunity lens that treats minerals strategy not merely as a defensive problem, but as a domain where American interests can actively be advanced.

The Policy Landscape: More Overlap Than Clarity

The federal government currently maintains multiple “critical” designations for minerals and materials, the most prominent being the **U.S. Geological Survey’s Critical Minerals List** (updated periodically under authority from the Energy Act of 2020) and the **Department of Energy’s Critical Materials List**, which tilts toward clean energy technology needs. Defense Logistics Agency lists prioritizations for the BAA, while a Congress.gov discusses congressional considerations as they pertain to critical materials, including a list of their own. These lists share significant overlap but differ in methodology, scope, and implied policy response.

What both lists share is a largely reactive character. They identify scarcity and import dependence, but they don’t readily answer the harder questions:

- How bad is our exposure?

- How quickly could an adversary weaponize it?

- What would it cost to change our position – and is that cost worth it?

China, by contrast, operates with a more integrated strategy. Beijing has pursued upstream resource acquisition globally (through the Belt and Road Initiative and state-directed investment), built dominant midstream processing capacity – particularly in rare earth elements – and is not shy about using that leverage diplomatically. Russia, while less globally integrated in this space, holds critical positions in nickel, palladium, and titanium, and has demonstrated willingness to weaponize resource access.

Why Prioritization Frameworks Matter

Not all critical minerals are prioritized the same. A useful prioritization framework needs to ask at least three distinct lines of inquiry:

- Supply risk: How concentrated is global supply? How dependent are we on imports, and from whom? How substitutable is the mineral, and at what cost?

- Demand trajectory: Is our consumption of this mineral rising or falling? How much of that demand is defense-critical versus commercial? What do projections look like over a 10- and 20-year horizon?

- Strategic leverage: Could an adversary restrict our access – and if so, what would the operational or economic impact be? Conversely, do we or our allies hold positions in this mineral that could be leveraged?

Current U.S. methodologies address supply risk reasonably well. They are weaker on demand trajectory and largely silent on strategic leverage in the offensive sense- the opportunity side of the ledger. A more complete risk/opportunity framework would score minerals not just on how exposed we are, but on where we have, or could build, genuine strategic advantage.

Allies, Partners, and the Geometry of Dependency

No minerals strategy makes sense in isolation. Australia, Canada, Japan, and the European Union are all developing their own critical minerals frameworks, and each brings different resource endowments, processing capabilities, and strategic priorities.

The Minerals Security Partnership (MSP), launched in 2022, represents a step toward allied coordination, but coordination is not yet integration. Ally and partner lists frequently diverge from U.S. lists, reflecting differing industrial bases and energy transition timelines. Mapping those overlaps and gaps is essential groundwork for any serious collective strategy.

At the same time, some of our most important potential partners in resource-rich regions- in Africa, Latin America, and Southeast Asia- are actively being courted by Beijing. The window to establish durable partnerships is not indefinite.

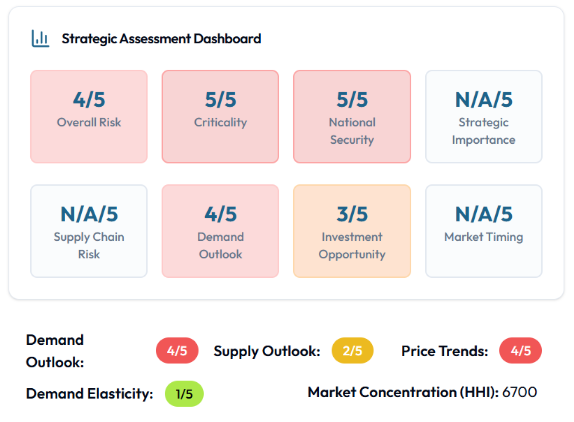

What our Risk/Opportunity Framework Looks Like

Imagine scoring each critical mineral across weighted dimensions. Our Critical Materials dashboard, Ellen, connects material-level risk and opportunity to mission-level decisions through SDA analytical frameworks. Key features of Ellen include:

- Ask Ellen: Ellen answers plain-language questions with sourced, action-oriented answers, grounded in vetted data.

- Risk & Opportunity Scoring: Every material is scored across 8 dimensions, so risk and opportunity are quantified, not debated.

- Continuous Monitoring: Emerging developments are viewed through an SDA-lens, ranked by consequence to separate signal from noise.

A composite score across dimensions yields a more actionable prioritization than import-dependence alone. It can also surface minerals where the U.S. is not primarily at risk, but where we hold cards worth playing.

This is the analytical foundation we’ll be building on throughout this series.

This post is part of an ongoing series on U.S. critical minerals strategy and national security.